The Current State of DeFi

Deep-dive into the lessons and progressions for DeFi to advance

Disclaimer: Any information posted on Polkastarter’s social media accounts shall not be considered personal investment advice or be construed as an express or implied promise, guarantee, or implication by Polkastarter that clients will profit from the strategies or that losses in connection therewith can or will be limited.

Author: @dariuskohsg

Editors: Antonis Kazoulis, Ami Tsang

The creation of Decentralized Finance (DeFi) has taken the crypto industry by storm and shaped the nascent industries by leaps. At its peak in December 2021, DeFi had garnered a whopping $247 billion total value locked (TVL) across multiple blockchain ecosystems.

Even though DeFi space has taken hits due to an increase in DeFi hacks and various tragic events, such as the failure of Celsius and FTX, DeFi has the most complete offerings that complement other sectors - namely, GameFi, SocialFi, ReFi, and more.

And if anything, the failure of the centralized finance mechanisms proves the importance of DeFi. Next, let us delve deeper to understand how much it has gone through and how much more it can still grow and evolve.

The Birth of DeFi: Uniswap

It all begins with a blog post shared by Vitalik on Reddit. He proposed an idea to run an on-chain decentralized exchange with automated market makers. This subsequently led to the birth of the DeFi industry.Although Bancor first developed the concept of liquidity pools, Uniswap popularized it for the masses and has become the backbone of today's DeFi.

Uniswap pioneered the:

i) Automated Market Maker model, in which users supply a set of two assets to Uniswap’s “liquidity pools” and algorithms set market price in place of an order book, where buyers and sellers create orders through brokerage firms based on supply and demand;

ii) Concentrated liquidity, which allows liquidity providers to select specific price ranges for which their assets are used to settle trades. As a rule of thumb, the tighter the price range you set for your liquidity, the more transaction fees you will earn when a trade happens in your range;

iii) Permit2 & Universal Router, which jointly allows users to abstract the approval process of the execution of multiple tokens/NFTs swap from various marketplaces in a single transaction, minimizing gas fees and greatly improving user experience.

Today, it has gained a foothold in the DeFi sector as the highest fee-generating protocol.

Notably, most of the mainstream cryptocurrencies have migrated to Uniswap V3, excluding long-tail assets.

What’s so special about Uniswap V3?

The defining idea of Uniswap v3 is concentrated liquidity: V3 pools allow users to supply their assets at a concentrated range along the price curve. This increases capital efficiency for the LPs whilst also improving the trading experience through reduced slippage.

More importantly, we observed that more projects have adopted Uniswap V3 as an infrastructure. By that, we do not mean those implementing liquidity mining with Uniswap Liquidity Pool (LP) ERC721 tokens but relatively much more advanced applications in the DeFi space.

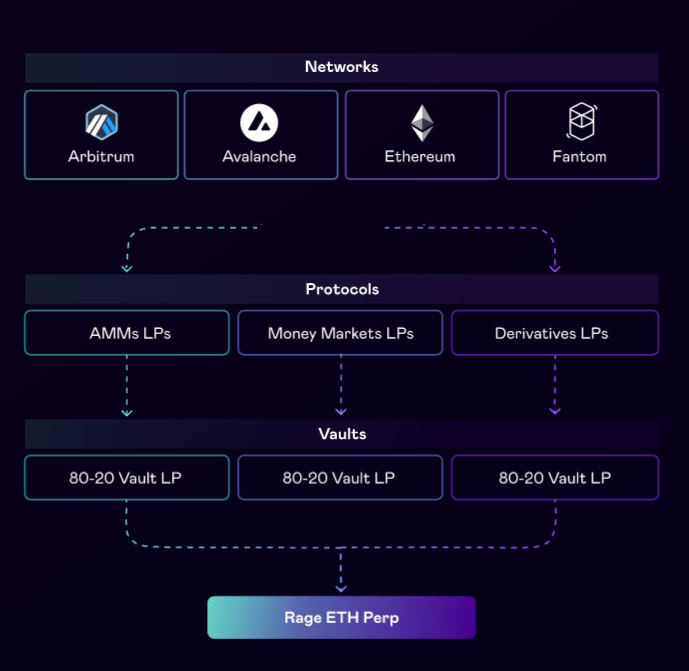

For example, Perp V2 and Rage Trade have tapped on UniSwap V3 to enable market takers to perform dollar-margined trading with up to 10x leverage. Rage Trade allows its users to recycle LPs from Uniswap V3 to provide liquidity by depositing their existing LP positions into their 80-20 LP vault and capturing additional yield on their LP position while replicating the payoff of an LP in Uniswap V2.

On the other hand, Perp V2 has also released its leveraged liquidity provision, which allows liquidity providers to choose different price ranges to provide liquidity to, and rewards are tied to the transaction fees they generate.

What Uniswap means to the DeFi industry is somewhat similar to the evolution path we see in Web 2.0 applications. Apps developed on Windows OS such as Chrome and Wechat included in-app applications and plugins. Similar trends can be observed in the Capital Market protocols, which we will dive into in the next section.

Capital market (credit borrowing and lending)

Unlike a traditional credit intermediary where a borrower needs to negotiate a loan maturity along with a borrowing rate, DeFi lending protocols reimagined this service in a trustless and automated manner to make lending accessible to all.Aave (ETHLend) & Compound: Pushing DeFi Lending ForwardThe two most significant borrowing and lending protocols - Aave and Compound - have respectively introduced multi-chain deployment in their V3. Here is what makes these protocols stand out.

Compound

Put simply, Compound is an autonomous protocol that calculates interest rates algorithmically. There are several reasons behind Compound’s success:

- No back and forth between lenders and borrowers: Unlike traditional lending processes where the borrower had to negotiate terms and conditions with the lender, Compound cuts out the noise and makes the whole borrowing experience seamless and lean.

- Makes investing easier: In a similar vein, investing becomes a simple affair on Compound. The ease with which users can borrow puts them in a position of power to profit from fluctuating interest rates.

When it comes to the challenges faced by the protocol, the most glaring one has to be market manipulation. Tokens that showcase diminished liquidity in open markets are vulnerable to price manipulation that could be exploited through the protocol.

Aave

Aave is an open-source protocol used to create non-custodial liquidity markets to earn interest on supplying and borrowing assets. To simplify it, Aave is a decentralized crypto lending platform that lets users borrow and lend crypto.

What makes Aave stand out?

- Non-custodial: Aave never really holds your cryptocurrencies. That means there is less risk of hacking and stealing funds as there are no wallers filled with funds.

- Flash loans: Flash loans are one of the protocol’s unique selling points, allowing users to take out a loan with very low fees and no collateral. The transaction is good to go if they repay the loan within a predetermined time period.

On the challenges side, one could argue that being tied to the Ethereum network and the associated high gas fees is something to consider.

The key issue with pool-based protocols like Compound and Aave is that they keep the utilization of capital low, so users can withdraw and borrow funds at any time. This causes a high spread between their borrow and lends APY, reducing the efficiency of the entire protocol.This has led to the emergence of Morpho Labs, a peer-to-peer-to-pool lending matching agreement based on Compound and AAVE that seeks to achieve a much higher utilization rate and, in turn, returns a better rate for both the borrowers and suppliers.

It is built so that if someone is not finding any counterpart via the P2P mechanism, Morpho falls back onto Compound/Aave by depositing the user’s funds in its smart contract. Under this configuration, Compound/Aave is considered as the supplier of last resort: the user is at least as economically rewarded as they would be by simply using Compound/Aave.

Another advance in the space is both Aave and Euler have introduced isolation-tier assets, which are available for ordinary lending and borrowing. Still, they cannot be used as collateral to borrow other assets. In other words, users cannot be borrowed alongside other assets using the same collateral pool. This helps to contain the damage from one underperforming asset or pool and not compromise the entire platform.

Uprising trend: DID-based non-collateralized lending

Since the start of 2022, we identified that the new critical innovations in the borrowing and lending sector are inter-institution lending and decentralized identifiers- (DID-) based non-collateralized lending.

Firstly, there are mainly two institutional streams of demand for capital:

- large market makers usually have an unlimited demand for capital and can borrow unlimited amounts to market-make as long as the APR is less than 10%, essentially making capital their tool of production.

- projects also need to issue debt and prefer to issue long-term debt to serve as their operating capital, but it is difficult for the crypto industry to have funders willing to issue long-term debt with low APR. A lack of positive project cash flows further aggravates this situation.

The borrowing and lending protocols should consider the two B2B streams as set out above. Two of the largest credit borrowing and lending protocols – Maple Finance and Solv Protocol – have re-pivoted to achieve so.

Secondly, DID-based uncollateralized or reduced-collateral lending is a much more ideal solution for the two B2B streams. Reducing collateral and improving capital efficiency by basing on one’s track record or reputation is much preferred by market makers and treasury managers.

However, DID development is still immature, so it’s too early to conclude whether a DID-based loan is a viable solution or a false proposition.

Decentralized Exchanges

There are two types of DEXs: Order book (Off-chain & On-chain) DEXs and Automated Market Makers. All of them allow users to trade tokens through their smart contracts, but they're based on slightly different principles.

Order books work well in traditional finance.

However, one can’t just transfer that onto the blockchain because of the associated high network fees and slow network speed, especially since many DeFi activities are taking place on Ethereum. That’s where AMMs come into play.

The table below summarizes the definitions, advantages, and disadvantages of different kinds of decentralized exchanges (DEXs) below.

What are the main problems with DEXs?

Now let’s explore the main challenges faced by decentralised exchanges.

Network congestion

The network congestion phenomenon occurs when the traffic flowing through a network exceeds its maximum capacity. In this scenario, it translates to traders’ inability to fill their trades and to market makers’ inability to cancel their positions. This rarely happens for some chains like Solana when NFT minting events occur.

Delayed Finality

Today, most blockchains, experience “probabilistic” transaction finality — meaning that transactions are not automatically or instantly finalized but become "more and more final" over time (as more blocks are confirmed).

Thus, transactions can still be potentially altered, reversed, or cancelled after completion.

Ideally, block times and transaction finality should be as short as possible.

Building challenges

Limitation of L1

If you’re building an order book on a smart contract on the L1, it is not possible to optimize the L1 to lead to the best performance for the order book. Why? Because DEXs are a particular type of application that have really high throughput and latency requirements.

Limitation of programming model (Serum)

Specific to Solana DEXs, their programming model only allows updates to a certain number of accounts per transaction. This is evident in Serum’s case where a user is not able to place a trade and get it fulfilled in one transaction. Nonetheless, optimizations on the L1 level can lead to much-improved user experiences.

2 Game Changers in the DEX world

dYdX V4 moving to Cosmos to create their own chain

dYdX is a leading order book decentralized exchange that runs on smart contracts on Ethereum. It currently operates on StarkEx, an Ethereum Layer 2 scaling network developed by Starkware.

However, it can currently only theoretically process transactions in the low thousands (perhaps it is only hundreds in actuality). This proves that a rollup to an on-chain order book-based DEX is not the final answer.In the dYdX V4 update made in June 2022, dYdX V4 will be developed as a standalone blockchain based on the Cosmos SDK and Tendermint consensus.

Moving to the Cosmos ecosystem to create its own blockchain, also known as an application chain (appchain), allows them to achieve the goal of building a fully decentralized protocol while ensuring high throughput and customizability.

Check out this article for an in-depth discussion about dYdX.

Sei Network optimizes block times, finality, and latency to make it fast

Sei Network is currently seeing 600 ms block times on their devnet with internationally distributed validators and 300 ms block times on the testnet with validators located in the same geographic region. Hence, it is the fastest blockchain in terms of actual finality.

In terms of throughput, Sei Network can process ~18,000 orders per second with 800 ms block times at present, which fulfills the requirement from an order book-based DEX standpoint.

By adding custom logic at the base level, the aforementioned three transactions can be done in a single transaction.

More details are discussed in Sei’s tweet.

What does it mean to be optimized for #DeFI?

— Sei (@SeiNetwork) October 4, 2022

Block times, finality, and latency are crucial when optimizing for financial applications. Sei optimizes for these from the ground up.

A thread on why Sei gives #DeFI an unfair advantage 👇🧵

Traders tend to stick to centralized exchanges (CEXs) for the following reasons: DEXs have their merits but using DEXs comes with challenges such as extra fees because of what’s paid to transact on-chain, network congestion, and slow speed.

The key trends in the DEX sector

Monopolism

Monopolism by the pioneering DEXs is evident in the sector. New DEXs with more novel and efficient AMM algorithms on the older chains couldn’t grab a piece of the market share. Only DEXs which are launched on the newer chains stand a chance to accrue Total Value Locked (TVL) and survive.

Gradual Infra-ization

As covered in an earlier section, another notable DEX trend is gradual infra-ization. This is where the blockchain's derivative protocols will rely on the liquidity of the bigger DEX to cover the demand of its users better. As a result, the DEX on the new chain will be able to dictate the liquidity of the spots and that of the derivatives in the future.

To break it down a bit more, infra-ization refers to the process of DEXs becoming the infrastructure layer. For example, you stake ETH and USDT into the Liquidity Pool and obtain ERC721. The ERC721 token can then be brought to other derivatives protocols to improve further capital efficiency.

DEX Aggregators

DEX aggregators help to solve the problem of fragmented liquidity. DEX aggregators source liquidity from different DEXs and thus offer users better token swap rates than they could get on any single DEX.

1inch is the leading DEX aggregator with more than $1.1 billion of 7-day volume at the point of writing. On both Ethereum and Polygon, 1inch is locked in a battle for supremacy with the 0x protocol, while Matcha is the 0x aggregator Dapp. Ultimately, the DEX aggregators game is one of bundling execution, which will be won on the parameters of fees, liquidity, availability of trading pairs, and, most importantly, integration of other Dapps and Protocols.

Why is 1inch well-placed to remain dominant in this space for the foreseeable future?

Aggregation can happen not only at the DEX/Dapp level but also at the network level. Since the competitors are essentially aggregating the same DEXs and Dapps across chains, this space is ripe for commoditization. Those attracting the most liquidity and offering the lowest fees will win. Execution and speed of adoption and expansion will be the key drivers for success.

What’s next for DEX aggregators?They have demonstrated a remarkable ability to extract capital efficiency from the DEX ecosystem and excellent execution in user acquisition and fund-raising. However, the rise of the alternate L1s opens up a new horizon for growth in two dimensions. The first is merely expanding the list of available DEXs and trading pairs.

The other, more complex path is through cross-chain swaps. One example is incorporating multiple chains and L2’s within the pathfinding algorithm. Another example is cross-chain staking - where a user can buy a token through a DEX aggregator in one chain and earn staking rewards from another.

Derivatives

Derivatives are a huge market in traditional finance and are no exception in crypto. In terms of advancements, the derivatives are not limited to the sharkfin products, dual-currency notes, and futures/options contracts on the blockchain. These decentralized exotic derivative protocols are bound to take a cut of the market share of Centralized Finance (CeFi), where the bulk of activity lies therein today. Also, some projects are exploring the possibility of structuring income streams of gaming guilds into derivatives.

Like DEXes, there is also a gradual infra-ization for existing decentralized derivatives protocol. For example, Cruize Finance is applying financial engineering involving perpetual swaps from dYdX to structure its downside-protected derivatives.

We believe that DeFi protocols will tap into existing derivative protocols as an infrastructure layer to tap into their already deep liquidity and structure more and more complicated exotic derivatives.

Stablecoins

Crypto regulations have made significant progress in 2022 and will continue to in 2023. Tether remains the leading stablecoin issuer, while Circle has been proactive in accepting compliance regulations and has slowly caught up to Tether regarding acceptance and usage. The pure algorithmic stablecoin UST also passed away in the year’s first half, representing the end of the pure algorithmic stablecoin narrative.

The adoption of a collateralized algorithmic stablecoin – FRAX, remains lukewarm. Notably, FRAX and DAI still hold a large proportion of USDC as their underlying collateral, i.e. the stablecoin sector is still being dominated by fiat-backed stablecoins.

DeFi giants like Aave and Curve have also announced that they would be working on over-collateralized fiat-pegged stablecoins as they look to verticalize and have a complete suite of product offerings in the realm of DeFi. AAVE stablecoin is expected to launch very soon, while Curve has just published the whitepaper for their new $crvUSD stablecoin on GitHub.

The future narrative of stablecoins would still be based on regulations and compliance hence much of the activity would be situated in the US.

Real World Assets (RWAs)

Naturally, the profile of RWAs differs significantly from traditional on-chain native assets.Intersections with the off-chain world through financing more traditional economic activity come with their own challenges. The opportunities, however, outweigh the challenges and create the potential for DeFi to create a more transparent and accessible global financial ecosystem.

Some of the most notable cases worth mentioning are:

1) MakerDAO’s collaboration with Centrifuge last year to provide DAI loans backed by real assets

2) MakerDAO’s investment into US treasuries and bonds with 500 million DAIClosing Thoughts"DeFi is the future." This refrain has been echoed amid the shocking events in 2022.

In our piece, we shared a sum of many moving parts, and DeFi as a whole is constantly adapting and evolving dynamically. We look forward to the next round of innovation in DeFi and Web3!

About Polkastarter

Polkastarter is the leading decentralized fundraising platform enabling crypto’s most innovative projects to kick-start their journey and grow their communities. Polkastarter allows its users to make research-based decisions to participate in high-potential IDOs, NFT sales, and Gaming projects.

Polkastarter aims to be a multi-chain platform and currently, users can participate in IDOs and NFT sales on Ethereum, BNB Chain, Polygon, Celo, and Avalanche, with many more to come.

Website | Twitter | Discord | Telegram | Instagram | YouTube | Poolside Podcast

Polkastarter Blog - Latest Polkastarter News & Updates Newsletter

Join the newsletter to receive the latest updates in your inbox.

{kind=link}