Polkastarter Is Bringing Back Low FDV Token Sales And Fair Community Launches

How Early-stage Fundraising Platforms Can Cure the High FDV/Low Float Challenges

We are facing a tough market right now… Bull cycle - checked. New promising projects launching - checked. Yet, recent token launches haven't performed as well as in previous bull markets. What’s happening? Are the VCs dumping on us or is it the team selling? Crypto Twitter is buzzing with this scenario.

The crypto market is evolving quickly. Institutional investors are now focusing on Bitcoin and a few blue-chip tokens and retail demand seems depressingly focused on meme coins. Public concern about startup fundraising is growing. Will the crypto market ever be as great for public backers as in 2021? How should future public fundraising in crypto look like?

In this article, we describe the challenges of the current market, exploring insights from experts Cobie and Haseeb Qureshi, along with data from Binance Research and CoinGecko. We focus on the pivotal role of early-stage fundraising platforms in the future of crypto fundraising.

We will also give examples of more balanced valuations and projects that are willing to be part of the change, projects like Lympid, a fully regulatory-compliant platform to issue and trade premium RWAs, that is launching on Polkastarter at a 12M fully diluted valuation.

High FDV/Low Float Challenges

In the current cycle, the high fully diluted valuations (FDV) and low float (low percentage of the total supply of tokens distributed on token release) launches became a norm. This situation is highly unfavourable for retail investors. High valuations and a limited amount of tokens in circulation pose a serious concern for smaller backers, significantly restricting their access to the new promising tokens.

Let’s break down the problem:

⚫ Private Capture and Phantom Pricing

As pointed out by Cobie in his analysis, in this cycle, significant price discovery happens in private markets before tokens are even available to the public. This often results in inflated valuations that don’t reflect true market demand. Teams, exchanges, and market makers leverage these private valuations leaving public investors at a disadvantage.

⚫ VC and Institutional Dominance

Haseeb Qureshi, managing a well-known crypto VC, acknowledges that venture capitalists capture most of the early-stage gains, leaving little upside for public investors. High initial allocations to insiders create significant sell pressure once tokens unlock. With no interest from the general public, early retail backers risk becoming ‘exit liquidity’ for private investors.

⚫ High Valuations and Low Float Trap

Many new tokens launch with high Fully Diluted Valuations (FDVs) and low circulating supply. The high FDV/low float setup restricts liquidity and meaningful price discovery. These tokens are often 'unbuyable' at launch - they only become available after unlocks and subsequent sell-offs. By that time, most of these coins exhibit discouraging downward trends and have already lost the attention of potential investors.

Low Float Crypto

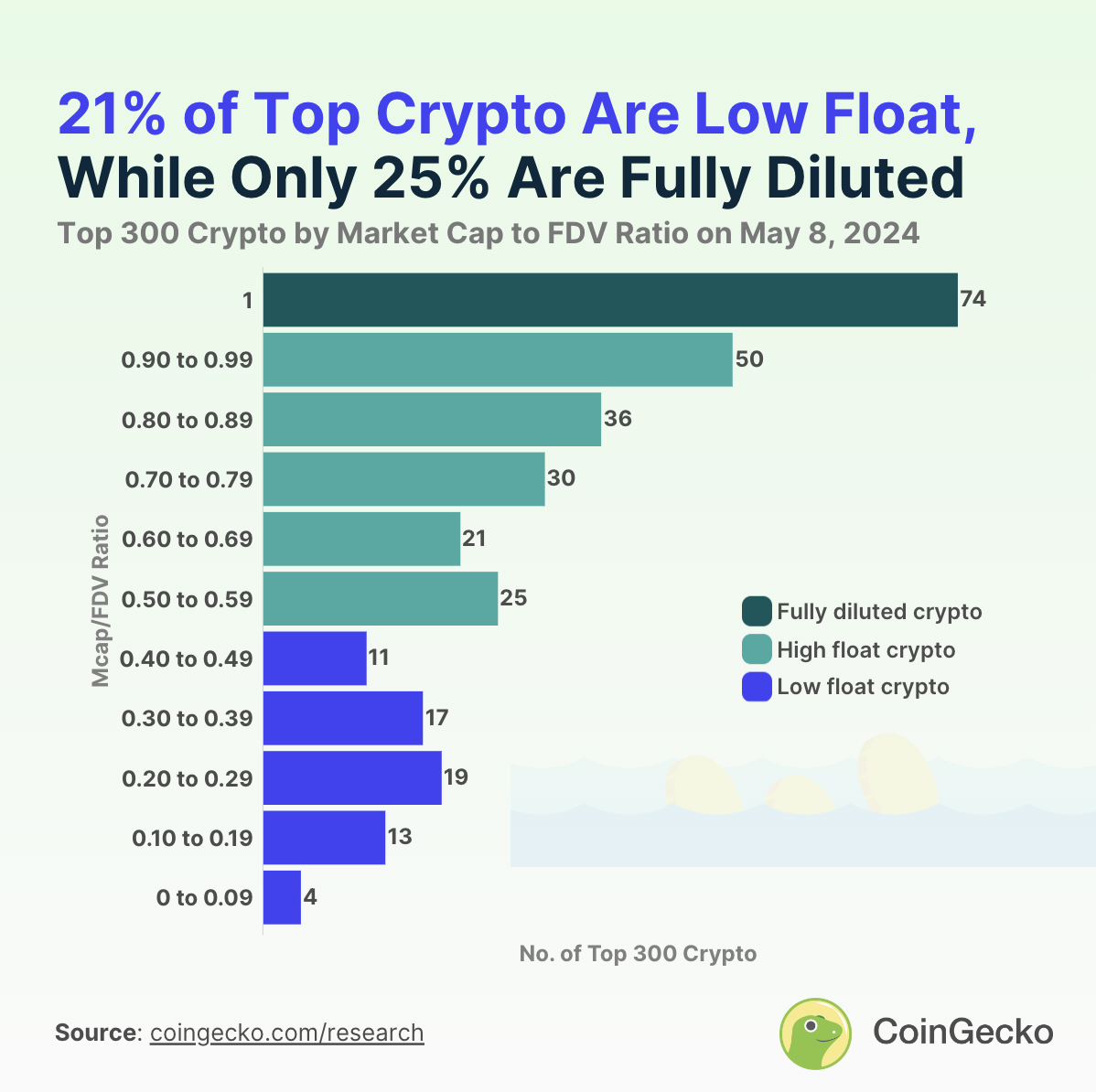

According to CoinGecko, low-float tokens make up 21.3% of the top 300 cryptocurrencies by market capitalization. Tokens are referred to as low-float if their market cap-to-FDV ratio is below 0.5, conveying that most of their supply is yet to be unlocked. Examples: Worldcoin ($WLD) - 0.02 ratio, Cheelee ($CHEEL) - 0.06, Starknet ($STRK) - 0.07, and Saga ($SAGA) - 0.09. Most low-float tokens are relatively new, having been launched in the last four years.

Binance Research estimates that around $155 billion worth of tokens will be unlocked from 2024 to 2030. Without a corresponding increase in buy-side demand, this substantial token supply will put significant selling pressure on the market.

In contrast, 54% of the top 300 cryptocurrencies are high-float tokens, with more than half of their supply already unlocked. These tokens generally show more stable price movements due to better liquidity and less supply overhang. Notable examples include Maker ($MKR) and Aave ($AAVE), both having a market-cap-to-FDV ratio close to 1.

High Valuations (FDV)

Valuations for private investors increased over time, along with projects' interest in raising capital from private entities. Public valuations surged even more, resulting in significantly smaller returns from public markets compared to past bull cycles and today's private returns.

To put it into perspective:

This increase in the metrics of private rounds led to unrealistic valuations at launch. Combined with a low initial circulating supply, this caused a decrease in public interest in new token launches. As mentioned earlier in this article, most gains are now captured in private rounds, leaving little-to-no upside for the community and public investors.

How Early-stage Fundraising Platforms Like Polkastarter Can Lead the Way

It’s not only the big-scale projects that fall short in this market. The chart below shows what percentage of all the projects launched publicly in 2021 and 2024 (till June) reach specific ATH range categories.

Smaller projects are subject to the same high FDV and low float failures as the big-scale projects, causing them to underperform at launch and miss their main chance to gain traction. The cure? Bring crypto fundraising closer to the public. Early-stage fundraising platforms like Polkastarter can help achieve this goal. With the community and public investors having a bigger stake in the token launches, projects can expect more stable and sustainable conditions.

David Lu shared in his X post:

“I believe community members that put skin in the game should be allowed to participate in as close to terms the latest private valuation. The reason is that many of these participants may have been with the project since Day 1 as a user or contributor. So why should they not be afforded the chance to participate at the same terms as the private investor?”

We cannot agree more. If the community of the project’s early supporters is unable to get an upside, what would make them stick around? In crypto, the community is a decentralised extension of the team, the project’s most valuable asset. Why subject them to a crazy high valuation?

We touched upon the fairness in token launches, going through the fundraising model evolution from Bitcoin to now in this article. In principle, crypto fundraising used to be FULLY public in the past. The ‘pre-mining’ and private allocation of tokens before launch was initiated with Ethereum (2014), but only recently have we started to see the long vestings and extended private investors' involvement.

We believe that early-stage public fundraising is the cure to the current market challenges of high FDV and low float, allowing for increased market fairness and more accurate price discovery by promoting public access to token launches.

Here’s why:

⚪ Transparent and Equitable Pricing

Moving forward, both the launching projects and fundraising platforms should prioritise transparency in pricing mechanisms. Prioritising public sales and opening private rounds to the public can help achieve fairer initial pricing. By allowing more public price discovery, projects and fundraising protocols can ensure that valuations reflect true market demand.

That is why at Polkastarter we conduct private sales for public investors and have community-driven sales on our 2025 Roadmap. We are not alone in this conviction: Binance Research recommends more public sales to achieve fairer initial pricing. Transparency in tokenomics and unlock schedules is critical, as highlighted by both Binance Research and CoinGecko findings.

⚪ Increased Circulating Supply at Launch

Successful fundraising via fundraising protocols should encourage projects to release a larger percentage of tokens at launch. This can enhance liquidity and improve price discovery. Gradual unlock schedules can stabilise the market. CoinGecko’s analysis on high float tokens supports the need for higher initial float.

⚪ Realistic Valuations

Launch FDVs must be based on realistic market assessments, aligning with the project’s stage and comparable metrics in the market. Establishing industry norms for acceptable FDVs and circulating supplies can help standardise expectations and improve investor confidence. Both Binance Research and CoinGecko underline the need for valuations to reflect true market demand and project maturity.

In our opinion, valuations of the public sales projects need to come back to around $5-10M pre-revenue and $10-20M for revenue-generating startups to be realistic and approachable for the community. It’s our goal to bring such low FDV projects to the Polkastarter community.

⚪ Investor Education

Fundraising protocols can educate investors about the implications of FDVs, tokenomics, and vesting schedules. Providing clear information about token distribution and fund usage can lead to more informed decision-making by the users. You can check this video by our research team on how to evaluate any token and our 101 introductory blog series. More materials will follow, so stay tuned. 📡

⚪ Governance and Variable Supply Models

Early-stage fundraising protocols can support the implementation of governance mechanisms that allow the community to vote on new token issuances. This provides flexibility and aligns token supply with the project's evolving needs and market conditions. Moving away from fixed supply models to variable ones can help manage supply overhangs and create a more adaptive economic model.

⚪ Community Building

One of the advantages of using early-stage fundraising platforms is their ability to help build a community of early supporters and maintain user engagement through community programmes and campaigns. For example, at Polkastarter we are soon releasing the Missions feature, allowing us to set up custom onboarding and engagement campaigns for launching projects and driving meaningful interactions. The Next LaunchLympid, as previously mentioned, embraces a sustainable approach to token launches.

Lympid is an established regulatory-compliant platform in Europe to issue and trade Real World Assets (RWA), offering a neo-bank-like app for investing in tokenised assets.

With Lympid, users can invest 24/7 in RWA with an easy-to-use app that gives access to assets like Horses, Art, Luxury Watches, US Treasuries and Residential Real Estate.

Within six months of tokenising the world's first show jumping horse called Doriano, Lympid returned profits of 70% to investors. There’s a lot more to come! They are launching a public round at $12M FDV with 50% unlock at TGE and only 2 months vesting.

Conclusion

Early-stage fundraising platforms can be crucial in establishing a healthier fundraising environment in crypto. With a focus on transparency, realistic valuations, equitable token distribution, and enhanced investor education, launchpads can create more robust and fair opportunities for both projects and investors.

At Polkastarter, we are in the best position to drive a fair and inclusive future for the crypto industry. That is our mission.

📚 Further read:

- CoinGecko Research report: here

- Binance Research report: here

- Milkroad podcast: here

- Haseeb’s article: here

- Cobie’s analysis: here

- Rob Hadick: here

- Davo’s post: here

About Polkastarter

Polkastarter is the leading early-stage fundraising protocol, enabling web3’s most innovative projects to kick-start their journey and grow their communities. Polkastarter allows its users to make research-based decisions to participate in high-potential public sales and be early to the future of web3.

Website | X | Discord | Telegram | Telegram Announcements | YouTube

Polkastarter Blog - Latest Polkastarter News & Updates Newsletter

Join the newsletter to receive the latest updates in your inbox.

{kind=link}